AUGUST 16, 2023 | Rayliant

The second quarter saw investors bidding stocks higher, swept up in a ChatGPT-inspired AI frenzy and encouraged by macro data pointing to a stronger-than-expected US economy. Meanwhile, fixed income markets came to terms with the fact that, despite a “hawkish pause” from the Fed in June, the central bank was unlikely to soon declare victory in its battle with inflation—made all too real amidst the heat by a recent Wells Fargo report, showing ice cream prices up 9% since last summer! Below, we highlight themes and data the team at Rayliant has been tracking as we turn our attention to the second half.

Rayliant Global Advisors is a global investment manager with offices in Los Angeles, London, Hong Kong, Hangzhou and Taipei. With over US$15-billion in assets linked to Rayliant's strategies, its clients include some of the world's largest sovereign wealth funds, pension plans, and other institutional investors. Rayliant's award-winning team is an independent advisor to East West Bank regarding global economies and markets. East West Bancorp, Inc. (the parent company of East West Bank) holds a 49.9% stake in Rayliant Global Advisors.

Quarterly Commentary: Asset Classes

Equities

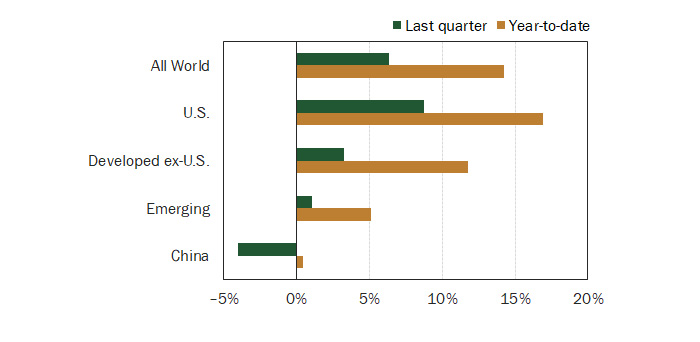

In the face of sticky inflation and rising central bank policy rates across most of the Western world, developed markets equities were ‘risk-on’ in the second quarter (see Figure 1). US stocks led the way, officially entering a bull market in early June and finishing the quarter up 8.7%, with gains concentrated in a handful of growth stocks. Concerns around the March banking crisis dissipated early in the quarter, and a potentially disruptive standoff over the debt ceiling resolved at the start of June without too much drama, removing some potential headwinds, while the Fed chose to pause last month, signaling to some that US policy rates may be near their peak.

Figure 1: Equity Market Performance (as of 30 June 2023)

(Source: S&P 500 (USD), FTSE All-Share (GBP), EURO STOXX 50 (EUR), MSCI Emerging Markets (USD), and CSI 300 (CNY), via Bloomberg as of Jun. 30, 2023.)

Developed markets outside the US ended the quarter 3.3% higher. UK stocks were an exception, falling modestly as a concentrated allocation to the energy and materials sectors suffered on concerns about China’s economic growth and due to pound strength on the Bank of England’s “reacceleration” of rate hikes. Japan, by contrast, was one of the best performers among developed markets, with the Nikkei 225 returning over 28% through two quarters, as strong balance sheets forged on the back of policies championed by the late former prime minister Shinzo Abe combined with a weakening yen have led to surprising earnings growth for Japanese firms. Emerging markets stocks rose by just over 1% in Q2, dragged down by China, whose tense relationship with the US and languishing zero-COVID exit recovery delivered a blow to sentiment.

As mentioned, growth stocks were the biggest winners among US shares in the second quarter, with the tech-heavy NASDAQ gaining 32% in the first half of 2023, its best start to a year in four decades. Indeed, excluding the so-called “Magnificent 7”—Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla—which have propelled the S&P 500’s year-to-date rally, the remaining 493 stocks would be roughly flat on the year. Among those top stocks, action during the quarter was truly astonishing. Nvidia, for example, blew Wall Street earnings forecasts out of the water at the end of May on the back of AI-driven demand for its GPUs, adding $207 billion in market value in just two days and flirting with trillion-dollar market cap status. Apple closed out Q2 with a string of four consecutive record-high closes, the last of which made it the first company in history to end a trading session over $3 trillion in market cap.

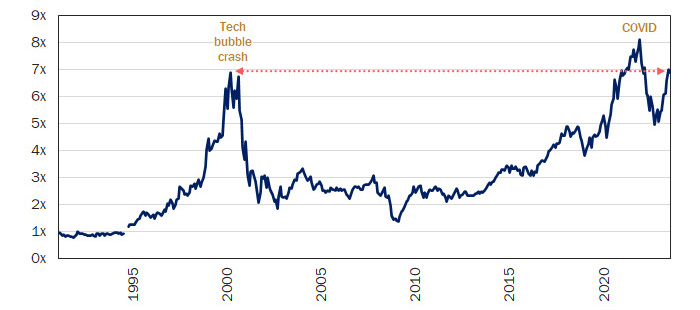

Investors witnessing such milestones have drawn comparisons with the run-up in tech stocks during the late-90s dot-com bubble, as surging valuations rewarded bull market believers while also setting a handful of stocks up for major corrections if future growth falls short of lofty expectations (see Figure 2). Enthusiasm around AI, in particular, has been a driving force behind the concentrated gains in US tech shares so far this year (see Figure 3), raising significant risk that hype outpaces reality, but also an opportunity to benefit from active selection as FOMO leads prices away from fundamentals.

Figure 2: Bull Market in Tech Drives Valuation Inflation

Through the first six months of 2023, stocks in the S&P 500 Information Technology Index climbed by nearly 43%. According to Bernstein analyst research, tech stocks now trade at around a 54% premium to the broader market: more expensive than they’ve been at any time in the last 45 years—except for during the late-90s dot-com bubble. We see a similar picture comparing prices to fundamentals. The tech sector’s price-to-sales ratio notched a lofty 7x to close out Q2, breaching levels hit in the run-up to the tech crash in early 2000. While there’s nothing to stop growth stocks from pushing higher still, such valuations obviously present a less compelling entry point than what investors faced at the beginning of 2023, while high prices leave much less margin for error if growth turns down.

Price-to-sales ratio of S&P 500 Info Tech. sector, Feb. 1991 – Jul. 2023

(Source: Rayliant Research, Bloomberg, as of Jul. 7, 2023.

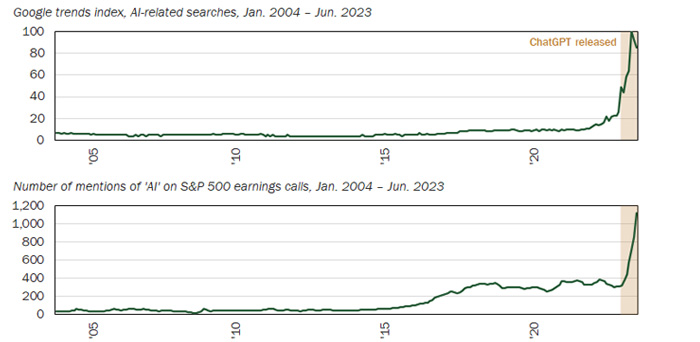

Figure 3: Underlying the ‘FOMO’ Tech Trade, a Surging Interest in A.I.

A big part of what drove the rally in tech stocks in the first half was an explosion in the public’s awareness around artificial intelligence, sparked by OpenAI’s release of its large language model, ChatGPT, at the end of last year. The service reached 100 million users in just two months, a feat that took TikTok nine months and Instagram over two years. By the second quarter, Google searches for AI were at record highs, mirroring investors’ enthusiasm for the theme. Meanwhile, S&P 500 firms wasted little time embracing that trend, plugging the technology in earnings calls at an unprecedented pace. While AI will surely fuel economic gains—Goldman Sachs estimates such advances could add nearly $7 trillion to world GDP in the next decade—judging by the hype, much of that may already be priced in.

(Source: Rayliant Research, Bloomberg, Google, as of Jun. 30, 2023.)

In thinking about what might derail this year’s rally, the most obvious candidate is a hard landing for the US economy, and a shallow recession remains our base case for the ultimate resolution of the Fed tightening cycle that began last March. We aren’t alone in that view. A survey by The Conference Board, published in May, saw 93% of CEOs polled forecasting a recession in the next 12 to 18 months, and the vast majority calling for a mild one. Bond prices are also flagging a downturn on the horizon, with an inversion in the Treasury yield curve that has persisted since last October and is now deeper than any witnessed since the early 1980s (see Figure 4). The average American, however, might not see it that way, as we note that Google searches for ‘recession’ peaked last June and, in the absence of an actual recession, have fallen back down to their long-term average (see Figure 5). Complacency around the risk of a contraction could likewise lead to some disappointment on the part of equity investors if Fed tightening continues until the macroeconomy rolls over and corporate earnings take a hit. As such, we remain cautious on US stocks with a preference for bargain hunting and quality growth.

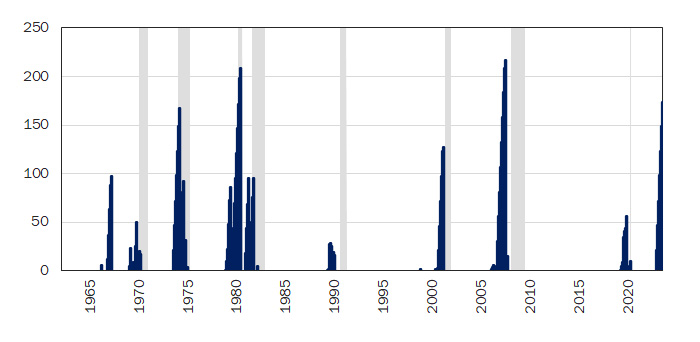

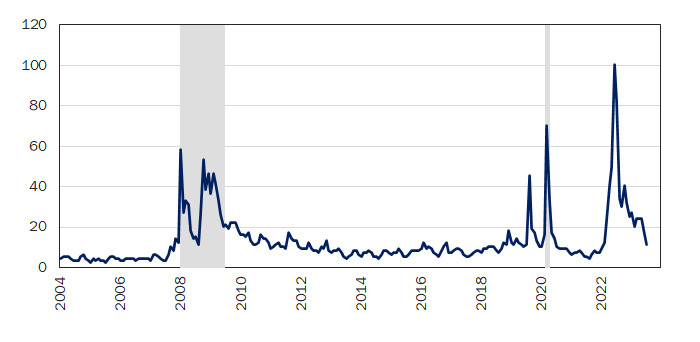

Figure 4: Recession-Watchers Asking “Are We There Yet?”

Despite equity investors’ enthusiasm as stocks break out of last year’s bear market, we still believe the most likely destination of fifteen months’ monetary tightening is some kind of hard landing for the US economy. The shape of the yield curve lends support to that view, with the spread between 10-year and 2-year Treasuries—an historically solid predictor of future recessions—as negative as it’s been since the early 1980s. Another way to look at yield curve inversion is with respect to how long it has persisted, and by that measure we’re on a pretty impressive run, breaching 170 trading sessions with a downward-sloping yield curve to end the quarter: the first time hitting that milestone since March 2007, and a sign of how long the wait for a much-anticipated recession has been.

Number of consecutive trading days with inverted yield curve, Jul. 1962 – Jul. 2023

(Source: Rayliant Research, Bloomberg, NBER recessions shaded, as of Jul. 7, 2023.

Figure 5: Last Year’s Anxiety Over a Downturn Fading Fast

Judging by web searches, the strength of America’s economy in defying recessionary yield curve forecasts seems for now to have allayed public concern over the future of US growth. In the first half of 2022, Google data show a massive spike in web queries related to recession, a pattern that lines up well with two contractions in US GDP experienced since tracking began in 2004. The expected recession never came and fears of a downturn gradually gave way, with recession-related search traffic falling back to its long-term average by last quarter’s end. While Googlers’ anxiety subsides, however, we see a risk of complacency. Even as search volume fades, The Conference Board’s May survey highlights the ongoing threat, with 93% of CEOs bracing for a recession within 18 months.

Google searches for 'recession', Jan. 2004 – Jul. 2023

(Source: Rayliant Research, Google, NBER recessions shaded, as of Jul. 6, 2023.)

Fixed Income

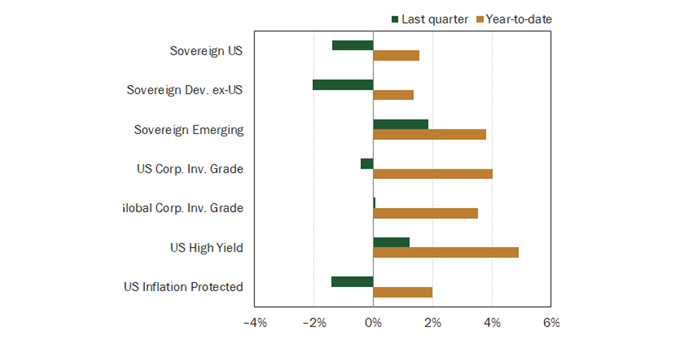

After a bounce back in Q1 from horrendous performance in 2022, bonds posted mixed results to finish the first half (see Figure 6), as most major central banks proceeded with rate hikes in their fight against inflation. Given the surprising strength of the US economy, which seemed ready to absorb the shock of further Fed tightening (see Figure 7), bond investors’ risk aversion waned throughout Q2, such that riskier bonds generally outperformed. Along those lines, sovereign emerging and US high yield were the best places to invest among those tracked here, returning 1.9% and 1.2%, respectively, for the quarter. Investment grade bonds were flat globally and modestly off in the US, declining just –0.4%. In sovereign developed space, US Treasuries returned –1.4%, as the Fed hiked at just one of two second quarter FOMC meetings, while developed ex-US performed slightly worse, consistent with the more concerning picture for inflation in Europe and greater hawkishness by European central banks.

Figure 6: Fixed Income Market Performance (as of 30 June 2023)

(Source: ICE US Treasuries Core, S&P Int. Sov. ex-US, JPMorgan EMBI Global Core, iBoxx USD Liquid Inv. Grade, Bloomberg Global Agg. Corp., iBoxx USD Liquid High Yield, Bloomberg US Gov. Inflation-Linked All Mat., all expressed in USD, via Bloomberg.)

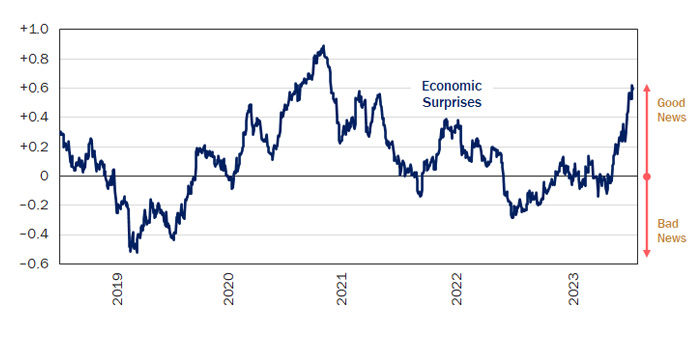

Figure 7: Positive Surprises Calm Investors’ Nerves, But Embolden the Fed

As experienced investors will recognize, not all news moves the market, and the market’s reaction to information can sometimes seem counterintuitive. What really matters is how surprised investors are by a report, and in what direction. In the second quarter, most surprises turned out to be happy ones for the US economy, as reflected in Bloomberg’s Economic Surprise Index, which tracks deviations from analyst forecasts for everything from CPI data and weekly nonfarm payrolls to consumer confidence surveys and housing starts. While America’s economic vigor no doubt helped investors to put worries of a recession on the back burner, we suspect a steady stream of robust data in Q2 also gave the Fed confidence to continue its restrictive policies, increasing the risk of an overshoot.

Bloomberg Economic Surprise Index, Jul. 2018 – Jul. 2023

(Source:Rayliant Research, Bloomberg, data cover Jul. 9, 2018 – Jul. 7, 2023.)

Indeed, investors feeling good about apparently moderating inflation in the US—June’s CPI represented the twelfth consecutive month of headline softening—might do well to consider the experience of other developed market economies and their central banks. One need not even go as far as Europe for a case study: Canada provides a good comparison, having actually beat the Fed to a ‘pause’ by six months, holding rates steady since the beginning of 2023. After accumulating data in the ensuing half year showing robust consumer spending, strong demand for services, and persistent tightness in the country’s labor market, the Bank of Canada chose to resume hikes in June, increasing its policy rate by another 25 bps in early July, with a further increase expected at the bank’s next meeting in early September. In a press conference after the July hike, Bank of Canada governor Tiff Macklem projected inflation won’t recede to the bank’s 2% target until mid-2025. Most major economies find themselves in a similar boat, with progress against core inflation increasingly hard to come by (see Figure 8), suggesting a tougher policy road ahead than many bulls might imagine.

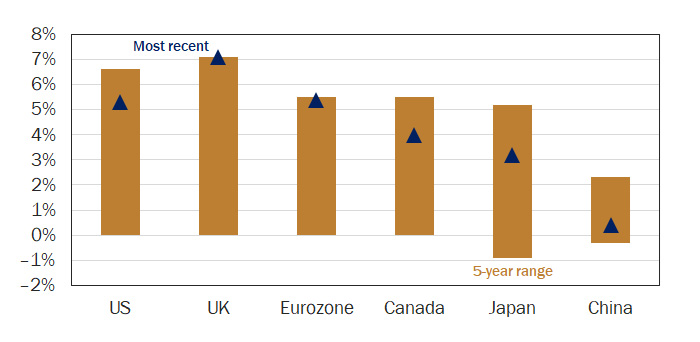

Figure 8: Core CPI Still a Bit Too Hot Across the Western World

Anyone following US inflation in the first half of the year—culminating in a softer-than-expected June CPI, marking the twelfth consecutive month of cooling and lowest reading since March 2021—might well conclude the Fed has rising prices in check and we’re on the fast track to rate cuts. In fact, stripping out food and energy, the US is in the same place most Western economies find themselves, with core prices still rising uncomfortably fast relative to history. That explains the Bank of Canada’s ending its six-month policy pause with a 25 bps hike last month, while the Bank of England put in a surprise 50 bps hike at its June meeting. By contrast, China faces lower-than-usual inflation, reflecting a stalling economic recovery and putting the People’s Bank of China squarely in easing mode.

Core CPI for various countries: Current vs. historical range

(Source:Rayliant Research, various countries' economic agencies, as of Jul. 7, 2023.)

In fact, we expect the Fed’s June decision was less a ‘pause’ and more of a ‘skip’, with a late-July hike almost a foregone conclusion at this point. We’ve been forecasting a higher terminal rate a long time, and the market is finally catching up with our thinking on this point, with Fed Funds futures now pricing in a terminal Fed Funds rate of just around 5.4% by November, implying another rate increase, which traders expect to happen at the July FOMC (see Figure 9). That’s a far cry from the prevailing consensus at the end of Q1 for summer rate cuts, as investors bet a banking crisis would soon shock policymakers into easing. We find it encouraging that yield traders seem more rational in their pricing of future Fed policy, though we expect the long end of the curve might continue to adjust as markets better bake in continuing Treasury issuance at increasing maturities as the US government replenishes the Treasury General Account and continues running budget deficits. At present, the degree of yield curve inversion combined with surprisingly tight credit spreads has led to some humorous occurrences in bond land, like corporate bonds trading at a premium to US Treasuries (see Figure 10)—though we suspect fixed income investors will mostly be happy in any case that they’re finally enjoying some ‘income’.

Figure 9: Traders Gradually Step Up Forecast of Peak Fed Funds Rate

After last year’s carnage in the bond market as the Fed aggressively tightened, many expected 2023 to be kinder to fixed income investors. Instead, outside of glimmers of hope for Fed rate cuts around the March banking crisis, the first half has been characterized by a gradual realization that Jay Powell means business. Indeed, since March 17th, futures traders’ expectation for the ‘terminal’ Fed Funds rate has risen over 150 bps, with the market now pricing in one more hike at the July FOMC, putting the peak policy rate at just around 5.4% by November. Given our view that the US central bank will keep rates ‘higher for longer’ and knowing that there’s a substantial amount of Treasury issuance on the horizon, we expect that bounce back in bonds could take a bit longer to materialize.

Anticipated terminal Fed Funds rate, Jul. 2022 – Jul. 2023

(Source: Rayliant Research, CBOE, data cover Jul. 7, 2022 – Jul. 7, 2023.)

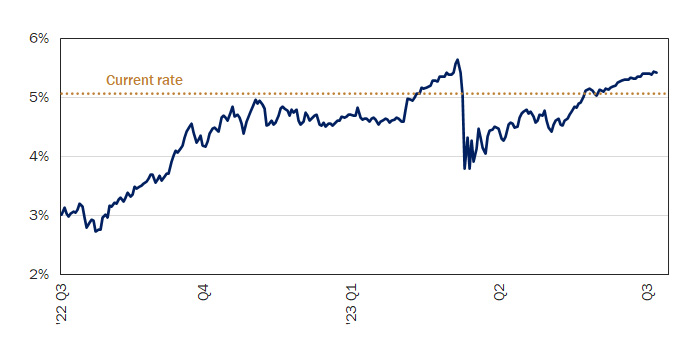

Figure 10: Treasury Yields Surpass Those on Corporate Bonds

Throughout the last year, in light of recession risk and what will likely be a further pickup in corporate defaults, we have noted the peculiar tightness of credit spreads. Consequently, there has been little to incentivize investors to take credit risk, as opposed to simply buying Treasuries and banking on the US government making its payments—notwithstanding an occasional debt ceiling crisis! The second quarter delivered yet more weirdness in credit markets, as the yield on 3-month T-Bills traded higher than that on investment grade corporate debt. Part of the disconnect results from corporate bonds having longer duration and lower yield given the inverted Treasury curve. As long as the Fed is threatening further hikes and spreads stay tight, Treasury bills may be hard to beat.

Bloomberg Aggregate Bond Index vs. T-Bills, Jan. 1997 – Jul. 2023

(Source: Rayliant Research, US Federal Reserve, ICE Bank of America, data cover Jan. 2, 1997 – Jul. 6, 2023.)

Alternatives

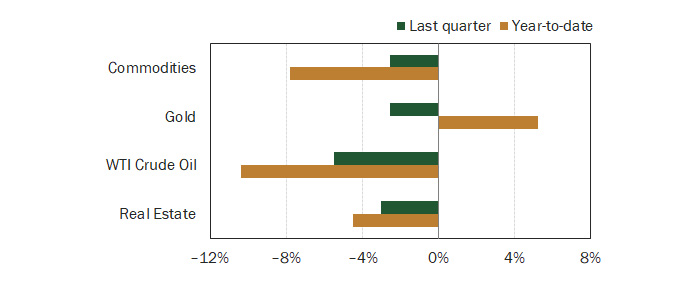

It was the second challenging quarter in a row for alternative assets, including property investments and a broad set of commodities (see Figure 11). Developed markets real estate slipped by –3% in Q2, bringing its year-to-date return through June to –4.5%. Within commercial real estate, growth in sectors that had been performing best post-pandemic—things like self-storage and multifamily housing—began to slow down in the second quarter, as higher rates, tighter CRE lending standards, and construction cost inflation took a toll. Despite that, fundamentals in the space remain solid, overall, with the hospitality and retail segments further improving, while office continues to struggle. Residential real estate in the US looked to be recovering in Q2, with new housing starts surging in May to their highest level in more than a year, up 18.5% month-over-month, and the National Association of Home Builders reporting in mid-June that that builder confidence had become positive again for the first time in eleven months. Such developments will be cheered by investors in single-family homes, after a first quarter that marked the biggest year-over-year contraction in the sector’s activity on record (see Figure 12).

Figure 11: Alternatives Performance (as of 30 June 2023)

(Source: Bloomberg Commodity Index, Gold Spot, WTI Crude, iShares International Developed Real Estate ETF, all expressed in USD, via Bloomberg as of Jun. 30, 2023.)

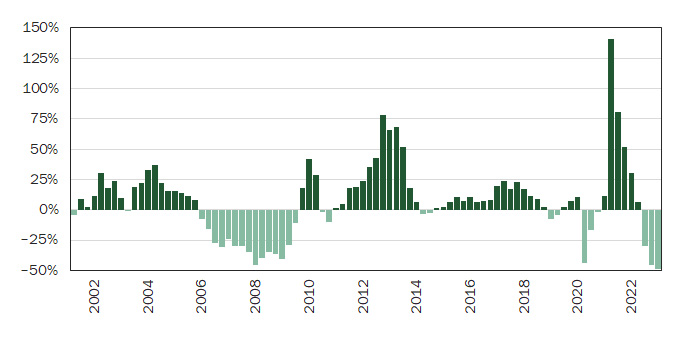

Figure 12: High Rates, Bleak Outlook Crater Investor Home Purchases

A real estate investment boom after the initial shock of the COVID pandemic saw triple-digit year-over-year growth in home purchases by individuals and institutions speculating in the property market, a record amount of activity according to data reported by research firm Redfin, compiled from county property records from Q1 2000. Rising rates over the last year, however, along with an uncertain economic outlook resulted in three consecutive quarters of declines in investor purchases, with the Q1 2023 representing the biggest ever year-over-year contraction. One problematic upshot for first-time homebuyers is that many of those investors who remain active have shifted their purchases to lower-price properties, further reducing the supply of affordable ‘starter’ homes.

Year-over-year growth in home purchases by property investors, 2001 Q1 – 2023 Q2

(Source: Redfin analysis of county records, as of Jun. 30, 2023.)

Commodities trended lower in the second quarter, as the prospect of further Fed tightening and signs of a global economic downturn—further fueled by continued evidence of a faltering recovery in China—weighed on demand expectations, with industrial metals and energy ranking as the biggest losers on the quarter. Copper’s Q2 weakness makes for a good example, as London Metal Exchange warehouse stockpiles hit an 18-year low in April—falling to less than a week’s worth of consumption—on hopes of a major boost from China’s zero-COVID exit, before surging by over 50% in May amidst big declines in copper prices, when it became apparent Chinese rebound was stalling. Despite this year’s setbacks for commodities, supply-side constraints in many sectors remain supportive of prices, while the demand picture could brighten fast if expected policy stimulus in China surprises to the upside and US dollar weakness as the Fed nears terminal rates inevitably becomes a tailwind (see Figure 13).

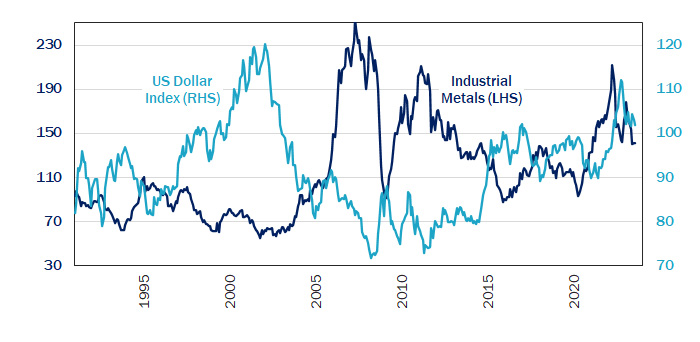

Figure 13: US Dollar Strength Adds to Metal Investors’ Woes

Industrial metals were among the poorest performers in commodity space in Q2, declining –10.5% for the quarter as China’s economic recovery fell far short of expectations that the nation’s zero-COVID exit might spur a rebound in demand for raw materials like aluminum and copper. Analysts at Deutsche Bank keenly observed that industrial metals’ second-quarter slump against the backdrop of a particularly strong US currency jibes with the historically inverse relationship between dollar strength and metal price performance. Those two headwinds could, of course, simultaneously reverse if policymakers in China come through with big stimulus and peak Fed tightening eventually gives way to a weakening dollar in the year ahead.

US dollar strength vs. industrial metal prices, Jan. 1991 – Jul. 2023

(Source: Deutsche Bank, Bloomberg, data cover Jan. 31, 1991 – Jul. 10, 2023.)

Economic Calendar

Key Economic Releases and Events for the United States – 2023 Q2

FOMC Rate Decision: 26th Jul., 20th Sep.

GDP Figures: 27th Jul., 30th Aug., 28th Sep.

PMI Figures: 1st Aug., 1st Sep.

CPI Figures: 10th Aug., 13th Sep.